LESSONS FROM THE NIFTY FIFTY

The Nifty Fifty Reminds Us That Valuation Eventually Matters

September 7, 2020

Click here to download the PDF version

LESSONS FROM THE NIFTY FIFTY

There are many ways to beat the market over long periods of time. Successful investors tailor investment strategies to align with their own set of strengths and weakness, cognitive and emotional biases, and frame of reference. Excess returns can come from many places, but do not come from owning winners at any price, buying high quality companies at any price, investing in category killers at any price or purchasing certain asset classes at any price.

GROWTH AT ANY PRICE

Growth stocks have trounced value over the past twelve months. The bifurcation between the haves and have nots has not been this extreme in a long time. Big winners are separated from big losers based on underlying business performance, irrespective of valuation. Investors are willing to pay almost infinite multiples for revenue streams that are insulated from the effects of COVID-19. Meanwhile, no price is too cheap for businesses that have been negatively impacted.

Long Duration

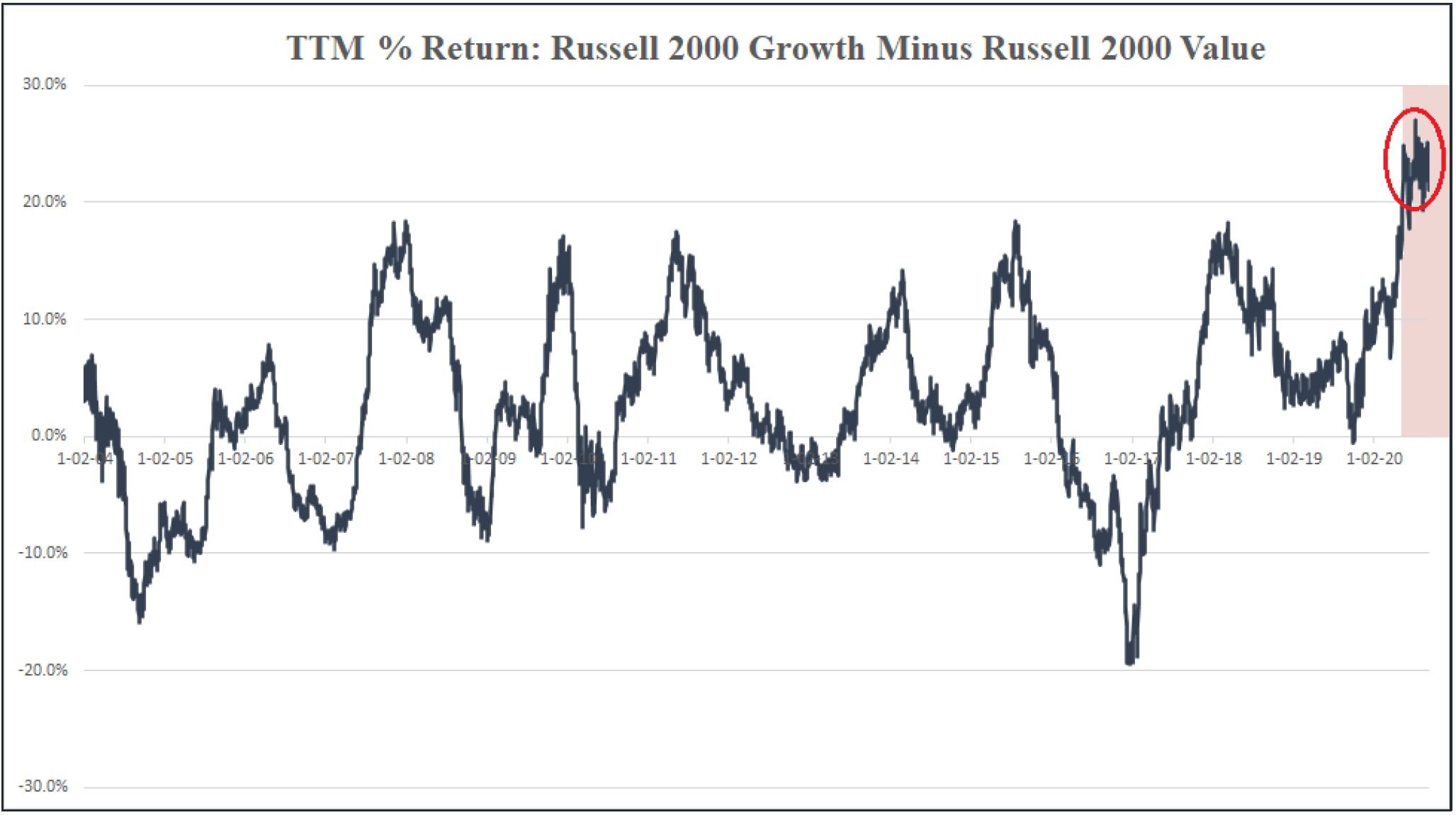

Below illustrates the TTM return differential between the Russell 2000 Growth ETF (IWO) and the Russell 2000 Value ETF (IWN). The one-year return delta right now is 21.1% (+13.4% versus -7.7%), the highest it has been since the dot-com bubble.

At a high level, this dichotomy can be easily explained. The seismic shift from value to growth is essentially a long duration trade. Permanent ZIRP plus low economic growth causes investors to sell short duration and buy long duration. Money-losing companies that are expected to generate significant profits at some undetermined point in the future when they own an entire market niche are said to be long duration. Reducing the discount factor towards the zero bound makes cash flows received in ten years more valuable relative to those received next year. Hence, speculative growth outperforms.

The problem is, at such expensive valuations, equity prices already reflect significant embedded optionality. When returns are expected to come from cash flows received a decade from now, investors can shape a narrative where trees will grow to the sky, and the notion of paying too high a price seems unimaginable. Limitless growth potential is always fiction and fundamentals often disappoint when investors extrapolate hockey stick growth for the foreseeable future. Not to mention, it is incredibly difficult to forecast that far out with sufficient accuracy. Narrative is more important for story stocks than numbers.

Fat Tail to Fat Tail

Growth stock outperformance is at a point along the bell curve last seen during the dot-com bubble. Rather than the creation of the internet, this extreme outlier phenomenon unfolded from a perfect storm of ultra-loose monetary policy, an explicit Powell Put, retail investors using helicopter money to participate in the most speculative areas of the market, and a gamma squeeze from large scale call option purchases.

Investor psychology is sensationally bullish. Recent news articles have suggested investors should end their obsession with valuation metrics, fractional shares are being introduced to retail investors who want to participate in the market but cannot afford to buy a full share, stocks of bankrupt companies have soared, ethical standards have collapsed, the market is headline driven, SPACs are in a mania, new metrics are invented to adjust for COVID-19, multiples are based on two or three years forward earnings, etc.

The point is that this kind of intense bullish speculation will probably not end in an orderly fashion. Instead, the momentum that has taken the market higher will likely reverse course in a violent fashion. In which case, that 21% delta outline above will be erased quickly, as the relative return profile jumps from one fat tail to the other fat tail before eventually mean reverting back to normalcy.

We recognize the growth trend may persist short term and nobody can know for sure when the tide will shift or what the catalyst will be. We would not rule out the possibility of a blow off top in the stock market. The divergence between growth and value can become much more extreme. It just means that the inevitable reversal will be more volatile. Either way, we suspect the outperformance of growth stocks will not continue unabated forever and feel confident that value will outperform over the medium to long term.

THE NIFTY FIFTY ERA

Nifty Fifty was a term used to describe the fifty most popular blue-chip companies on the NYSE between the late 1960s and early 1970s. Investors considered purchases to be a one-factor decision at the time: Were these the highest quality businesses with best long-term growth prospects? If yes, buy the stock.

Investors correctly identified winners within the market but failed to adequately assess the valuation risk incurred from owning shares. Most of these stocks traded in excess of 50x EPS and subsequently crashed by more than 80% from the peak. The Nifty Fifty group severely underperformed the broader market from 1972 to 1982, despite impressive earnings growth over those years.

Price Matters

The key lesson from the Nifty Fifty is that a great company could become a poor investment if purchased for way too much money. This misconception existed because investors believed risk was determined by quality instead of price. The relationship between value and price is the most important concept for fundamental investors to understand. Below average assets can be above average investments if they are cheap enough, and vice versa.

Future stock prices are a function of forward earnings per share and the multiple applied to those expected earnings. Money can be made by identifying stocks with rising earnings and multiples. At a minimum one of those factors needs to remain constant while the other rises. But money is lost when both of those variables shrink.

P/E Contraction Offsets EPS Growth

A great company becomes a poor investment when multiple contraction offsets robust EPS growth. Nifty Fifty companies grew earnings much faster than the market for a decade, but the P/E ratio fell enough to more than offset strong underlying business performance, resulting in lower stock prices. The same thing happened after the dot-com bubble when high quality technology companies underperformed the market for years despite enormous EPS growth. Certain companies did not see their stock price reach the 1999 peak for another ten or fifteen years.

The false assumption during the Nifty Fifty era was that there was no price too high to own a piece of one of the most spectacular companies in the world. Valuation risk no longer applied because the current situation was somehow different than what was experienced in the past. It was believed that these handful of blue-chip companies were the future and their dominant market positions would somehow insulate investors from any losses irrespective of price paid.

Similarities to Today

Investors decided to own a specific subset of stocks irrespective of valuation. That statement describes today’s environment as much as it describes the Nifty Fifty era. The combination of the Powell Put plus zero percent interest rates for the foreseeable future has given investors the impression valuation risk no longer applies today either. This time is different because rates are at zero, so valuation multiples have no upper bound. There is no price too high for business models that will benefit from the pandemic and enjoy multi-year tailwinds as a result.

Bubbles are always built on grains of truth. COVID-19 may permanently restructure parts of the economy. The internet did change the world. Housing prices do go up over time, on average. Junk bonds did, at some point, overcompensate bondholders for credit risk. The Nifty Fifty companies were mostly wonderful businesses. But in each of these instances, investors became solely focused on fundamental risk, ignoring valuation risk completely and it did not end well.

VALUATION EVENTUALLY MATTERS

We remain dedicated to our process and our investment style. We believe that staying disciplined, especially at times when it is hardest to do so, will ultimately pay off. Being a value-oriented investor during periods where narrative-driven story growth stocks outperform by an extraordinary margin is not easy, but we feel strongly that this kind of divergence will not last forever.

Valuation eventually matters, even with rates at zero, and should be the starting point for value investors. Price paid determines long-term prospective returns. Eventually could come in three weeks, three months, or three years. Investor psychology can dictate short-term prices, but fundamentals and valuation dictate long-term prices. The obvious winners in this environment are priced for perfection. Chasing these highflyers to infinity times earnings feels intellectually dishonest as the prospective returns on this subset of stocks are likely paltry over the next three to five years.