LONG IDEA - COLLIERS INTERNATIONAL GROUP

Colliers International Group (CIGI) Long Thesis

December 10, 2020

SUMMARY

Colliers is a high-quality compounder hiding in plain sight. A long overdue multiple re-rating combined with strong organic growth, margin expansion, and M&A suggests many ways to win.

INVESTMENT THESIS

Multiple re-rating candidate. The core business has transformed its revenue composition from primarily cyclical, low-margin sources to high-margin, recurring value-added services. CIGI is a prime candidate for a multiple re-rating given close to 60% of forward EBITDA will come from recurring revenue streams.

Strategic investments provide runway for long-term growth. CIGI is creating a unique platform of numerous commercial real estate and related offerings. Combining adjacent and new market verticals can create revenue synergies by cross-selling services between these subsidiaries. Further, the new verticals have highly fragmented end markets where Colliers can take share and pursue tuck-in acquisitions to enhance its growth profile.

High insider ownership and long history of creating shareholder value. Insiders own approximately 25% of the economic interest and 54% of the voting share. Shareholder value creation has been unlocked in a variety of ways including organic growth, strategic acquisitions, and spin-offs. Jay Hennick, Chairman and CEO, has demonstrated a commitment to maximizing shareholder value for decades.

INTRODUCTION

Colliers is a deeply underappreciated high-quality compounder, in our view. The company is dual listed on the TSX and Nasdaq under the symbol CIGI. Our thesis is relatively straightforward.

In short, the business has undergone a multi-year strategic shift and has transformed itself from a low-margin, cyclical, and commoditized business into a business that generates 50% of sales, and more than 55% of EBITDA, from high margin, recurring revenue streams.

We feel this strategic shift is overlooked by investors and, as the business continues to grow its recurring revenue segments, a pending change in perception will warrant a multiple re-rating. Going forward, we estimate more than 50% sales and almost 60% of EBITDA will be recurring in nature, which suggests this tipping point may be soon.

Long-term we believe the business has significant growth opportunities ahead of it. CIGI is building out a unique platform of numerous commercial real estate related services which deepen its economic moat and provide growth opportunities in both adjacent markets and new market verticals.

COMPANY BACKGROUND

Colliers was founded by Jay Hennick, who still serves as the CEO and Chairman. Hennick owns all of the outstanding multi-voting shares and controls 43% of the total votes. He has proven to make shareholder friendly decisions in the past, such as the spin-off of FirstService Corporation (FSV) in 2015. Hennick, along with the other insiders, own an economic interest of 25% and control 54% of the total votes.

Historically, the company relied heavily on its commercial real estate Sales & Lease Brokerage business. Colliers was successful at building a name for itself and has grown sales from $340 million in 2000 to $3 billion in 2019 (plus an additional $2.4 billion if you count FSV).

Sales & Lease Brokerage is generally a low-margin, cyclical, and commoditized business that warrants a relatively low valuation multiple. Colliers has undergone a strategic shift to focus their business on higher margin, recurring revenue streams such as Outsourcing & Advisory and Investment Management.

The street still views Colliers as the same business it used to be, and this misconception presents an opportunity for those willing to dig beneath the surface to really understand the vision Colliers has of their future.

BUSINESS SEGMENTS

Colliers primarily operates in three business segments:

Sales & Lease Brokerage (50% of sales) – Leasing, Capital Markets

Outsourcing and Advisory (44% of sales) – Project Mgmt., Valuation, Prop. Mgmt., Loan Servicing

Investment Management (6% of sales) – Advisory, Incentive Fees, Transaction & Other

Segment #1 – Sales & Lease Brokerage

This segment is what investors typically think of when they hear the name “Colliers.” This segment tends to be lower margin and very cyclical. It has been hit hard from Covid-19. Colliers does not break out EBITDA by segment, but we estimate normalized margins to be ~11%.

Segment #2 – Outsourcing and Advisory

This segment is significantly underappreciated by investors, in our view. This segment posted 2.7% y/y growth in 9 months ended September 2020, despite Covid-19. We believe this speaks volumes to the recurring and non-cyclical nature of its revenue streams. Colliers does not break out EBITDA by segment, but we estimate normalized margins to be ~14%.

Segment #3 – Investment Management

The Investment Management segment is relatively new, and Colliers entered the space by acquiring Harrison Street in 2018. Colliers does not break out EBITDA by segment, but we estimate normalized margins to be ~36%.

Segment Growth Rates

The Outsourcing & Advisory Segment grew top-line sales at an annualized rate of 16% between 2015-2019. It’s difficult to parse out segmented data going further back than 2014 because Colliers’ reported revenues included FirstService. The Outsourcing & Advisory segment also managed to post low-single-digit growth this year amidst a global pandemic, a feat we feel reflects well on the company’s management team.

Outsourcing & Advisory and Investment Management not only possess more attractive investment characteristics from a revenue reliability, EBITDA margin, and cyclicality standpoint, but both were growing at a faster rate than Sales & Lease Brokerage before the pandemic as well. This shift in revenue composition is no accident.

STRATEGIC TRANSFORMATION

CIGI’s strategic shift has been underway for years and we believe the revenue and margin profile of the business is approaching a tipping point where the successful transformation will be impossible to ignore. The progress since 2010 is undeniable and analyzing the company’s EBITDA margin paints a clean picture.

Colliers increased EBITDA from $27 million in 2010 (3.2% margin) to $359 million in 2019 (11.8% margin). Increasing EBITDA dollars 13x while quadrupling EBITDA margins over the past ten years is impressive on its own, but the company also managed to grow the recurring portion from 31% in 2017 to 57% in 2020.

EBITDA margin expansion combined with the increased portion of recurring EBITDA is driven largely by the company’s changing revenue sources. Sales & Lease Brokerage comprised of 66% of revenues in 2014 vs. 50% today. Outsourcing & Advisory comprised of 34% of revenues in 2014 vs. 44% today. Investment Management accounted for zero revenues in 2014 and comprises of 6% of revenues today. See below.

Colliers is far less geared towards the underlying real estate than it used to be, especially since adding Harrison Street, Dougherty, and Maser Consulting to their platform. Most of the CRE business is now recurring as well.

This trend in revenue mix shift is still ongoing and, in our view, has a long runway ahead of it. As a larger portion of the company’s revenue and EBITDA come from recurring sources, analysts will be forced to value the entire entity on a sum-of-the-parts basis and assign a more appropriate valuation multiple to each segment.

Today, most analysts assign a price target based on a company-wide EV/EBITDA multiple derived from CIGI’s historical trading range which does not appropriately reflect the positive fundamental changes to the business model over the years. We believe assigning a price target today, when recurring revenues are 50% of revenues, based on the stock’s previous trading range, when recurring revenues were only 34% of revenues, significantly undervalues two out of three business segments.

LONGER-TERM VISION

Colliers does not explicitly lay out their strategic vision for the next 5-10 years, so this section is mainly our interpretation from reading between the lines. The company is clearly gravitating towards higher value-added services that carry better margins, have less cyclicality, and minimal capex requirements.

It appears to us Colliers has already laid the foundation to build out a platform of related commercial real estate services that can drive meaningful revenue synergies going forward. Cross-selling is probably not the right word but offering services in adjacent markets allows them to increase revenue capture with existing clients.

Long-term, Colliers’ decision to enter new market verticals goes beyond revenue synergies from complimentary service offerings. These new market verticals provide a valuable growth engine for the company going forward. We believe the management team intends to take share in highly fragmented markets and pursue tuck-ins to further enhance the growth profile of the overall business.

Shareholder Value Creation Through M&A

Colliers “big three” strategic investments over the past few years were (1) Harrison Street, (2) four subsidiaries of Dougherty Financial, and (3) Maser Consulting. These acquisitions, explored in more detail below, provide Colliers with a suite of new service offerings and give Colliers a foothold in a variety of new end markets.

Harrison Street

Harrison Street appears to be the most transformative deal. The recurring nature of the business’s revenue stream is underappreciated, in our view. Roughly 50% of AUM is in open-end evergreen funds, meaning revenue generated from these perpetual structure vehicles are truly recurring, provided there are no significant redemptions. The other 50% of AUM is derived from closed-end funds with average fund lives between 8-10 years. Harrison Street is consistently raising money for new closed-end funds to offset maturing funds.

Growing AUM is only the first step to unlocking shareholder value from this acquisition. Real estate assets managed by Harrison Street provide Colliers with an enormous pipeline to drive growth in the rest of their segments.

Colliers can offer services when any underlying assets need to be purchased, sold, or leased; needs a valuation opinion or property management services; requires a loan or debt financing; or if any assets need consulting/engineering services. Integrating these businesses and leveraging this unique platform could unlock meaningful shareholder value long-term.

Dougherty Financial Subsidiaries

Colliers acquired four subsidiaries from Dougherty Financial, a debt finance and loan servicing platform. The interesting part is this acquisition came with a DUS license (Delegated Underwriting & Servicing). The DUS Program grants approved lenders the ability to underwrite, close, and sell loans on multifamily and senior living properties to Fannie Mae without prior Fannie Mae review.

The opportunity for Colliers, specifically, is this license grants them the ability to provide debt for all the transactions they do in the multifamily, senior living, student housing, and affordable housing space. So, on top of getting a brokerage fee on the placement of that debt, Colliers can also earn fees to originate the debt and then additional revenue from servicing it over the following 20 years. The cross-selling opportunity is enormous on its own. The additional sticky revenue generated from servicing Fannie Mae loans for the next two decades is the real kicker.

Maser Consulting

Maser Consulting provides a variety of engineering and design services in real estate and infrastructure end markets. We believe the decision to enter this new market vertical gives Colliers an incredible growth opportunity that is largely neglected by investors. Beyond the obvious revenue synergies from integrating Maser into Colliers’ platform, this acquisition presents an opportunity to take market share and pursue tuck-ins in highly fragmented end markets.

Colliers has already demonstrated their ability to create value by organically taking share in fragmented industries and bolstering that process with shrewd tuck-ins. The potential growth runway is long and, if Colliers can successfully run the same playbook with Maser, this segment could provide a tailwind to earnings growth for many years.

Unique Platform

Without getting too lost in the weeds about each individual acquisition, the main point is this. Colliers has a strategic vision for the future of their business. The management team is deepening the business’s economic moat, improving growth prospects, and increasing the reliability of its cash flows as activities are diversified away from the traditional commercial real estate sales and leasing brokerage.

This symbiotic relationship between the base business and the above acquisition targets will improve revenue synergies short-term. But the real opportunity is longer-term in nature. Colliers is transforming its business; its future growth prospects are bright, and investors continue to underestimate the company’s long-term earnings potential. The Colliers of yesteryear was transactionally focused on commercial real estate deals. Colliers is de-emphasizing that part of the business as they become closer to a one-stop-shop for anything real estate related.

COMPOUNDER WITH HIGH INSIDE OWNERSHIP

We believe the management team possesses the necessary expertise to successfully implement this long-term strategic vision. Key decision makers appear to be properly incentivized to execute effectively.

Colliers is a Traditional Compounder

Any way you spin it, Colliers has been a compounder for decades, and Jay Hennick has been at the helm the entire time. Most long ideas are complimentary of existing management teams and reference anecdotal or qualitative data. But, in this case, the results speak volumes.

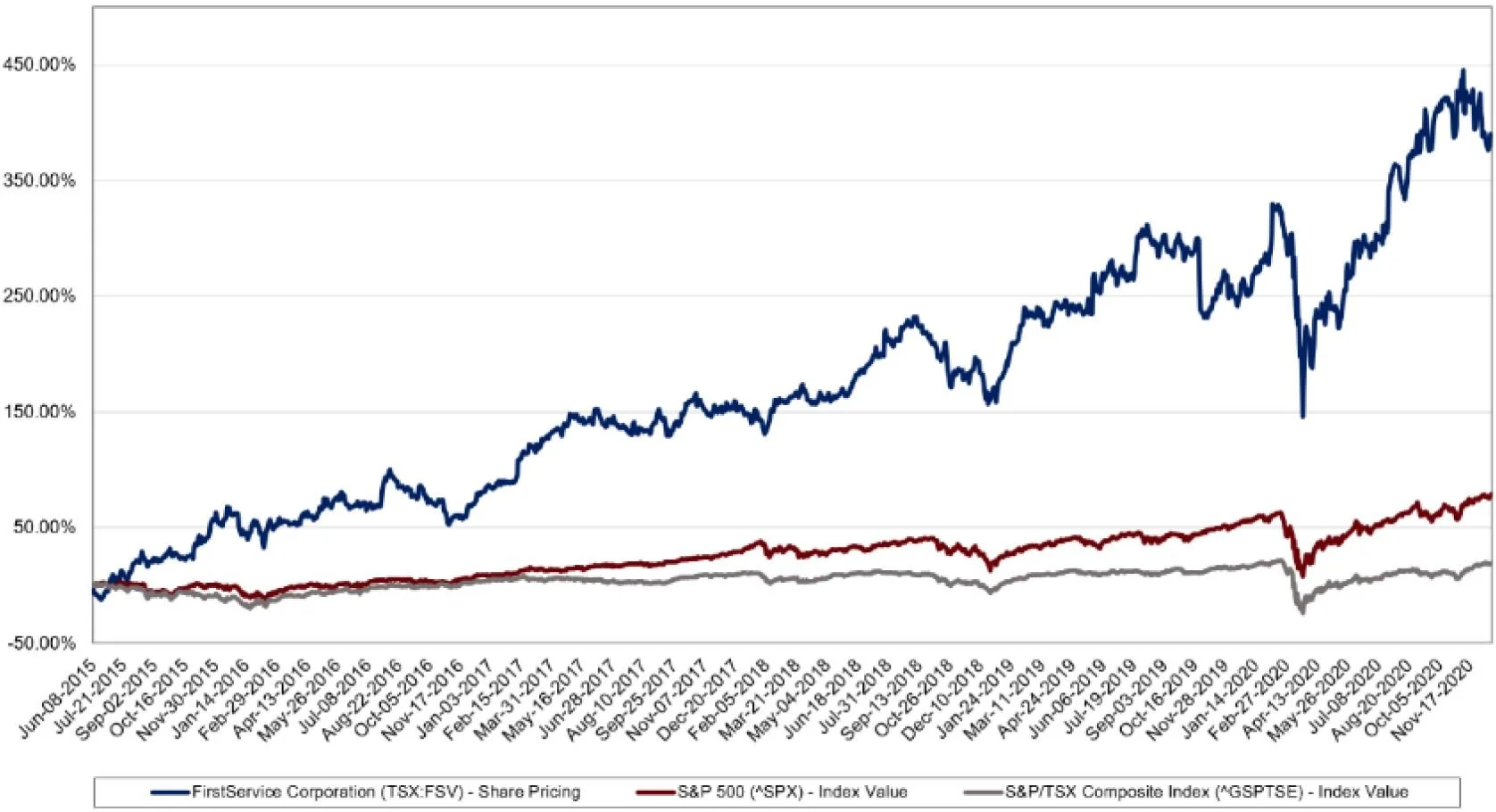

FirstService Corporation Spin-Off

Not only has Hennick demonstrated his ability to compound capital but, just as importantly, he has demonstrated a willingness to prioritize what is best for shareholders. Colliers made the decision to spin-off FirstService Corporation into a standalone entity in 2015 and appoint a separate CEO to lead the business. Below illustrates how well FirstService has performed post-spin.

Inside Ownership

Hennick, along with the rest of the management team and board members, have significant skin in the game. We feel this aligns their interests with those of the shareholders. Key decision makers at the firm have a vested interest in driving the share price higher. High inside ownership alone does not eliminate certain risks such as overpaying for acquisition targets, excessive use of leverage, or engaging in other value destructive behaviour.

But, when combined with other elements of our thesis and a strong corporate culture, it leads us to believe the management team is far less likely to recklessly swing for the fences to goose annual performance bonuses.

It is worth noting Hennick owns 100% of the outstanding multiple voting shares (1,325,694 shares outstanding). Spruce House is an investment management firm with board representation through Benjamin Stein. Another large investment firm, BloombergSen, owns another 5% of the shares outstanding according to their most recent 13-F filing. This concentrated ownership situation reduces the shares available for float.

VALUATION

We believe CIGI should be valued on a SOTP basis by assigning different multiples to their (1) Sales & Lease Brokerage segment and (2) Outsourcing & Advisory and Investment Management segments.

Sales & Lease Brokerage: The closest public company comparable for this segment is Marcus and Millichap (MMI). MMI is skewed more toward investment sales, more profitable during the good times and less profitable than the bad times. We believe CIGI’s Sales & Lease Brokerage segment should trade roughly in line with MMI at 10x EBITDA.

Outsourcing & Advisory and Investment Management: Finding a clean comparable for this segment is more difficult. Instead, we gauge its worth by its underlying investment characteristics. These segments grow organically at mid-to-high single digits plus tuck-ins, have recurring revenue during recessions, strong EBITDA margins, and generate a ton of FCF due to minimal capex requirements. We believe, given today’s ultra-low-rate environment and pricey stock market, this segment should trade for at least 16x EBITDA.

ESTIMATES

Below are our forward estimates for Colliers.

Key Assumptions

We estimate the Sales & Lease Brokerage segment will fully recover by 2023. This assumption may prove to be overly conservative but, given there is so little available information about the trajectory of the recovery, we prefer to model conservatively and be surprised to the upside.

We anticipate the Outsourcing & Advisory / IM segments will rebound quickly next year, and that momentum should carry forward for the next two years with a combination of organic growth and tuck-in acquisitions.

Our margin assumption for the Sales & Lease Brokerage business is 11% and a blended 15% margin for the Outsourcing & Advisory and Investment Management segments. We feel this assumption is realistic and we are not pricing in overly aggressive margin expansion in the coming years.

It is worth noting that our estimates are fairly in line with sell-side expectations. We believe there is a degree of conservatism in these forward numbers and any surprises are more likely to be to the upside than the downside.

PRICE TARGET

Below is our sum-of-the-parts analysis for approximating a fair value for CIGI shares in CAD. We believe upside is substantial given the low prospective return investment landscape. Further, it’s not often that high-quality compounders have more than 20% upside in one year and almost 40% upside over a two year holding period.

CATALYSTS

Multiple re-rating. We believe the primary catalyst for CIGI will be a change in investor / sell-side perception of the business. Again, the “Colliers” brand is still perceived to be a low-margin, cyclical sales & leasing business. When recurring revenue contributes more than 50% of revenue and almost 60% of EBITDA, this misconception becomes practically impossible to ignore.

Continued earnings growth and M&A. Continued organic earnings growth and additional value creation from M&A activity. Colliers has been busy in the M&A market and tends to make shrewd deals, in our opinion. We believe the company is more likely to make tuck-in acquisitions to bolster top-line revenue growth, rather than large transformative acquisitions.

Recovery in Sales & Lease Brokerage segment. Additional potential upside from a faster than expected recovery in the Sales & Lease Brokerage segment. We have no view of where commercial real estate prices are going in the short-to-medium term. That said, Colliers is less geared towards the underlying asset value. Sales and leasing volume – not price – is the critical factor. The company gets paid when activity occurs, regardless of transaction price. Even if commercial real estate value declines, we believe the volumes will eventually return.

RISKS

Continued weakness in the Sales & Leasing Brokerage segment. A second wave of the virus could potentially result in a continued impact on transaction volumes throughout 2021.

Execution risk. There is always execution risk any time a business is undergoing a strategic transformation. That said, we feel the management team has done a fantastic job so far which bodes well for the future.

Potential value trap. A key tenet of our thesis is a pending multiple re-rating. There is no guarantee the investment community will share the same opinion on the quality of the Outsourcing & Advisory or Investment Management segments. In that instance, a multiple re-rating would be unlikely.

Slowing growth in Outsourcing & Advisory and Investment Management segments. Should these segments stop growing, due to company-specific or market related factors, the valuation multiple applied to the whole business could contract.

Low float can result in choppy trading patterns. We estimate a significant percentage of common shares outstanding are closely held and do not frequently trade. This can cause volatility uncorrelated to the market.