Q1 2024

Kinsman Oak Investor Letter Q1 2024

April 25, 2024

Click here to download the PDF version

COMMENT ON PERFORMANCE

The Fund and its individual underlying holdings performed relatively in line with our expectations except for Tidewater (TDW), a recently initiated long position, and the unnamed offshore driller we mentioned in our last investor letter. We were fortunate enough to get a starter weight before the stock rallied +36% from our average cost. We continue to own the stock.

Modest detractors include longtime holding Churchill Downs (CHDN) and Nike (NKE). Our thesis on Nike was straightforward. We believed sentiment towards their China segment was overly negative and we anticipated a near-term inflection. A beaten down high-quality business with an upcoming catalyst combined with the stock trading close to its trough valuation multiple made for a potentially interesting set-up, in our view.

Our thesis turned out to be somewhat correct and the stock traded higher after-hours when the company reported results. Unfortunately, we underestimated how challenged the rest of the business would be from a competitive standpoint, and gains were quickly erased after the management team provided underwhelming forward guidance. This was a classic instance of missing the forest for the trees. As such, we exited our position.

MARKET COMMENTARY

Risk appetite was strong during the first three months of this year. The fear of missing out was palpable, meme stocks are back in fashion, and even SPACs have returned with a vengeance. The Levkovich Index is once again firmly in euphoric territory for the first time since early 2022 (Appendix A). Clearly, speculation is running hot, and the stock market is behaving as if interest rates were zero.

Investors anticipated six rate cuts at the beginning of the year which was quickly reduced to three by the end of the quarter. Since the March CPI data recently came in hot, many are now beginning to wonder whether we will get any cuts at all. To put it in perspective, this marked the 36th straight month of inflation clocking in above 3% and the 2nd straight monthly increase. The S&P 500 and Russell 2000 are down -5.3% and -8.2%, respectively, in April.

The consensus narrative might be changing from immaculate disinflation coupled with rapid rate cuts to a more realistic expectation of strong nominal economic growth, persistent inflation, and higher-for-longer interest rates, or some combination thereof. We expect increased volatility throughout the narrative shift.

We are admittedly surprised at the continued strength of the economy. In fact, economic indicators have been so good lately, executives have resorted to blaming the weather for poor business results. In our opinion, citing the weather for drastic underperformance without quantifying its precise impact is a strong signal that replacing the management team is probably the most expedient path to shareholder value creation, but we digress.

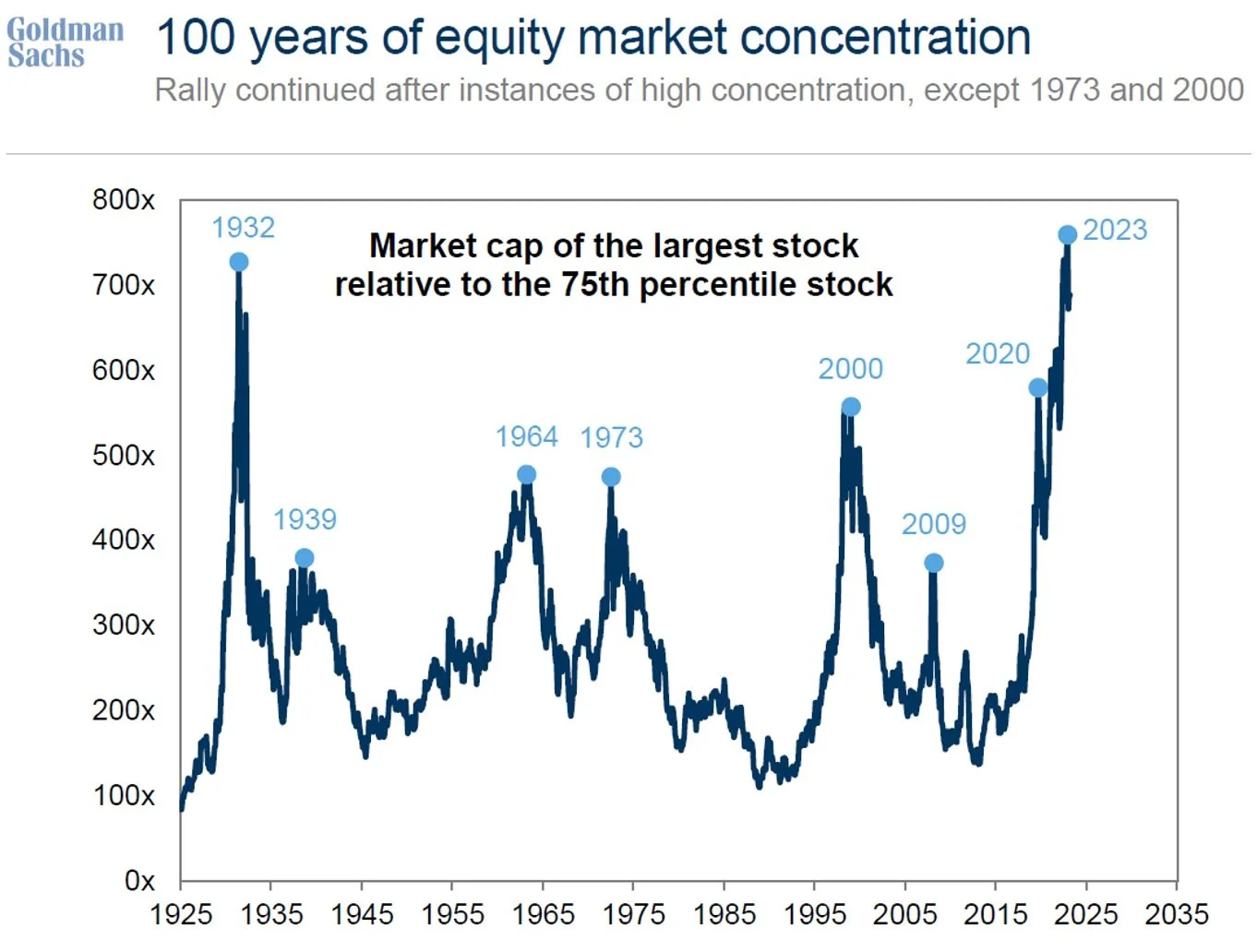

The stock market remains historically concentrated, albeit the magnitude is down slightly from recent highs (Appendix B). Over the past six months, and despite the rally, the S&P 500 has experienced declining FY24 earnings expectations. Specifically, the Magnificent 7 have had positive EPS revisions while the remaining S&P 493 have had negative EPS revisions, putting the index in net-negative territory on aggregate (Appendix C). Returns for the technology sector have trounced the index by more than two standard deviations, an even larger degree than what was experienced during the dot-com bubble, statistically speaking (Appendix D).

ALPHABET AND AI

Alphabet (GOOG), a longtime holding in our Fund, stirred up considerable controversy earlier this year when the company released their proprietary AI tool called Gemini to the public. Suffice it to say, the images generated were historically inaccurate and the extreme political leanings of its creators were not even remotely subtle. On the one hand, we decided to maintain our position and do not expect this event to negatively impact near-term results. On the other hand, we also believe this poses a serious risk to the incredible economic moat surrounding its core search business and early warning signs for the potential erosion of that moat are worth paying close attention to.

Alphabet was quick to suspend the use of Gemini and went into full damage control mode after the botched rollout. In an effort to mitigate reputational damage, the company cited poor training models, apologized for its shortcomings, and admitted that they “definitely messed up.” Despite the official theoretically plausible explanation, we suspect their artificial intelligence product is working as designed and the outputs generated were exactly as intended, reflecting a specific ideological agenda of Alphabet’s employees.

Last week, CEO Sundar Pichai, published a blog post titled Building for Our Future AI which outlined some internal operational and structural changes, and more broadly discussed his vision for artificial intelligence. Below are two excerpts from the last paragraph that particularly stood out to us (emphasis added):

We have a culture of vibrant, open discussion that enables us to create amazing products and turn great ideas into action. That's important to preserve. But ultimately we are a workplace and our policies and expectations are clear: this is a business, and not a place to act in a way that disrupts coworkers or makes them feel unsafe, to attempt to use the company as a personal platform, or to fight over disruptive issues or debate politics. This is too important a moment as a company for us to be distracted.

We have a duty to be an objective and trusted provider of information that serves all of our users globally. When we come to work, our goal is to organize the world’s information and make it universally accessible and useful. That supersedes everything else and I expect us to act with a focus that reflects that.

The first excerpt clearly addresses Alphabet’s severe corporate culture issues. We are encouraged Sundar Pichai recognizes he is responsible for running a business and employees need to be mission-oriented at the office. However, extreme cultural issues are exceptionally difficult to fix. Presumably the organization has layers upon layers of middle management filled with individuals who share the same radical political beliefs. How do you force an overwhelming majority of activists to be more moderate?

Disney is dealing with similar internal issues that have already had meaningful negative consequences to business performance. Elon Musk reportedly had to fire approximately 80% of employees after acquiring Twitter, partly due to inefficiencies and because the business was hemorrhaging cash, but also partly due to ideological incompatibilities. The point is, recognizing it is one thing but executing a turnaround is more challenging.

The second excerpt addresses the inherent biases programmed into Gemini and perhaps other Alphabet products, including legacy search. We are again encouraged Sundar Pichai envisions the creation of an artificial intelligence solution that strives to provide objective and apolitical information to its end users or, at the very least, maintains the perception of doing so. Again, this is easier said than done, but this blog post gives investors some indication that the management team is aware of potential reputational damage and is focused on preserving the valuable moat the business has spent decades building.

Artificial Intelligence & Competitive Advantages

Our perspective is that any competitive advantage AI provides will eventually have less to do with raw processing power or the calibre of programming embedded within the code itself. Instead, the competitive advantage will be determined by the degree of perceived bias sprinkled into the results. End users will gravitate towards AI programs they can trust. In other words, users will prefer when the output generated is compatible with their preexisting and often subjective interpretation of reality.

Alternatively, we can envision a future where AI becomes heavily regulated. In such a scenario, we assume winners and losers will be selected based on the preference of whichever lawmakers and politicians are responsible for writing and enforcing applicable policy. In either case, we do not believe a natural monopoly would exist under purely free market conditions.

GOLD

Gold reached a record high of USD 2,342/ounce on April 12th and is one of the best performing major asset classes year-to-date (+14%). Market sentiment remains bullish, and the upward trajectory shows little signs of slowing down despite being clearly overbought. The shiny yellow rock has a reputation for being perpetually unloved by the masses while being treated somewhat like a religion by the faithful minority.

At its core, the metal is essentially a tangible asset without a yield. Owners do not collect dividends or receive coupon payments for possessing it. In fact, the opposite is true since there are generally annual storage and insurance costs associated with holding it (unless you secretly bury it in your backyard). As such, investors tend to gravitate towards gold in times of low and negative real interest rates since the opportunity cost is relatively lower.

What is particularly interesting about the recent move higher is the historical correlation between the spot price of physical gold and real interest rates has further decoupled (Appendix E). Real yields on the U.S. 10-Year have increased from ~1.6% to ~2.0% since the beginning of the year, accompanied by a reduction in rate cut expectations. All else equal, we would have expected this dynamic to put downward pressure on the price of gold based on its prior directional relationship with real interest rates. But, instead, the price has gone up in a steep, straight line.

This decoupling began approximately mid-2022, intensified during 2023, and now the historical relationship between these two variables appears to be completely inverted, in our view. Gold prices and real interest rates are both rising simultaneously which is unusual and suggests there may be a significant paradigm shift worth exploring. The timing of the initial decoupling coincided with a confluence of related events which we suspect contribute to this gradual inversion.

In essence, the Federal Reserve started to aggressively hike the Fed Funds Rate while the federal government passed one massive spending bill after another. The ballooning annual fiscal deficits piled onto an already gargantuan national debt and, all of a sudden, U.S. net interest payments as a percentage of annualized government receipts skyrocketed from ~8% to ~18% (Appendix F).

Recent hotter-than-expected inflation data suggests real interest rates will likely remain higher for longer. If deficit spending continues to be recklessly irresponsible (which we assume it will be), then the annualized percentage of government receipts earmarked for interest payments will continue to climb as well – and practically guarantees escalating budget deficits in subsequent years. This self-reinforcing process can quickly spiral out of control barring some combination of interest rate cuts and fiscal restraint, and even that may not be enough.

In our opinion, the parabolic price of gold suggests investors and other central banks believe this trajectory is unsustainable, and the complete inversion of a longstanding historical relationship is simply more evidence of that. The structural fiscal dilemma will only get worse the longer real interest rates remain elevated. And as this dilemma gets worse, the future likelihood of extreme monetary accommodation, yield curve control, outright debt monetization, premature interest rate cuts, etc. increases accordingly. We believe this largely explains why both gold prices and real interest rates are rising simultaneously.

Taking Advantage of Rising Gold Prices

There are a few ways to take advantage of this theme. The first, and most boring option, is to get exposure to physical gold. The second option is to buy gold mining stocks which is less than ideal in an inflationary environment. While the price per ounce goes up, so do the costs associated with extracting it from the ground. Generally, owning the miners can be thought of as a leveraged gold position but the sector has significantly lagged performance-wise due to higher costs (Appendix G). Side note, the bull case on most gold mining stock is basically the same. They all have the best management team in the business and own the best assets in the world.

The third option is to find unique and off-the-beaten-path individual stocks that benefit from rising gold prices, and there are really only a handful of options. We ultimately chose the most boring and least volatile way to hedge against what we would consider monetary insanity (GLD). Our view was hitting a reliable single was preferable to swinging for the fences because, if we were right, our prospective risk-adjusted returns would be satisfactory.

LOOKING AHEAD

Numerous crosscurrents will determine which direction the stock market and the economy are headed from here. Plenty of unanswered questions will come into focus as the year progresses. For instance, can economic growth remain strong? Can valuations continue to withstand higher interest rates? Can profit margins remain strong if inflationary pressures weigh on cost structures?

We believe the business, economic, and credit cycles all remain in uncharted territory, so we remain open to a wider range of possibilities than most. Investors are thirsty wanderers navigating through the desert, and prospective rate cuts remind us of a mirage on the horizon. Always maintaining the illusion of being near but, the closer you get, the further away it becomes.

We expect intermittent bouts of volatility as the competing crosscurrents engage in a high stakes game of tug-of-war. Financial markets are inherently reflexive, so we anticipate a strong possibility that the foreseeable future will be a fat-tailed environment, meaning outsized upside/downside risks. This means we will attempt to opportunistically capture upside moves and hedge aggressively when we feel it may be appropriate.

Sincerely,

APPENDIX

Appendix A - Citi Research – The PULSE Monitor – April 19, 2024

Appendix B – Goldman Sachs – Where to Invest Now – April 2, 2024

Appendix C – Goldman Sachs – Where to Invest Now – April 2, 2024

Appendix D – B of A Global Research – The Flow Show– March 21, 2024

Appendix E – HSBC Global Research – Gold Outlook – April 10, 2024

Appendix F – Jefferies – Greed & Fear – April 11, 2024

Appendix G – Bloomberg